Download slides

Download slides

Capacity discipline and network shifts define February

Published: Thursday, February 05, 2026 | 09:00 AM CDT

Onthispage

Soft demand masks capacity constraints

February often carries a reputation as a more subdued month for ocean freight—a temporary pause between the intensity of pre-Lunar New Year shipments from Asia and the early spring ramp-up. At first glance, this year may seem to follow that familiar pattern. Rates in several major lanes appear steady or even soft, and broader global demand trends may give the impression of a market catching its breath.

But a closer look suggests a more nuanced picture. While the broader market environment appears calm, February is compressing several forces at once: accelerated pre-holiday demand, reduced post-holiday capacity, ongoing congestion at key global hubs, and routing decisions that introduce wider transit-time variability. These aren’t dramatic disruptions on their own, but together they may create a narrower planning window than surface-level indicators imply.

A month defined by timing rather than demand

February typically revolves around the timing of Lunar New Year which starts February 17 this year. As factories wind down ahead of the holiday, bookings pull forward, schedules tighten, and space becomes less predictable. Then carriers historically reduce sailings to align with lower factory output—reductions that have typically ranged from 30–45%, creating a temporary contraction in service and pushing some delays into March.

An added consideration this year is the overlap with Brazil’s Carnival (February 16–17), which may further limit capacity across both Asia and South America during the same week. While neither event alone is destabilizing, the overlap adds timing sensitivity to both regions.

Stability driven by capacity discipline

The market’s current stability may be more a function of deliberate carrier actions than a sign of underlying equilibrium. Carriers have been closely managing supply through blank sailings and targeted service changes. These efforts can make the market feel stable, but also mean fewer alternative sailings when weather, port slowdowns, or missed cutoffs occur.

This reduced margin for disruption is visible in regional operating conditions. In North America, shippers are front-loading imports to beat Lunar New Year slowdowns, causing short-term inland pulses in drayage, chassis, and distribution network capacity—even as overall import volumes remain below last year.

Routing choices are adding new variability

Another factor shaping February is the divergence in carrier routing strategies. Some services—such as the CMA CGM INDAMEX and Maersk’s MECL service strings—have returned to the Suez Canal, restoring shorter transit times, while others continue diverting ships around the Cape of Good Hope, leading to noticeably different arrivals on the same trade lanes.

These routing shifts do not necessarily disrupt planning, but they increase the range of possible transit times. As a result, the specific service string—and the routing it follows—matters more for reliability than the port pair alone. For shippers operating with tight production timelines or just-in-time inventory models, this environment may require additional buffer time—particularly on routings involving multiple transshipment points or recently adjusted service rotations.

On certain lanes, the gap between scheduled and actual arrival windows appears to be widening, elevating the importance of service-string selection and proactive coordination through the post-Lunar New Year period.

Schedule reliability not improving

In February, global schedule reliability still faces headwinds, not just due to changes in routing. Reports show that on-time arrivals in major shipping routes are lower than usual. Delays are caused by longer wait times for transshipments at busy ports, weather problems in northern Europe, and the ripple effect of blank sailings, which force more cargo onto fewer ships.

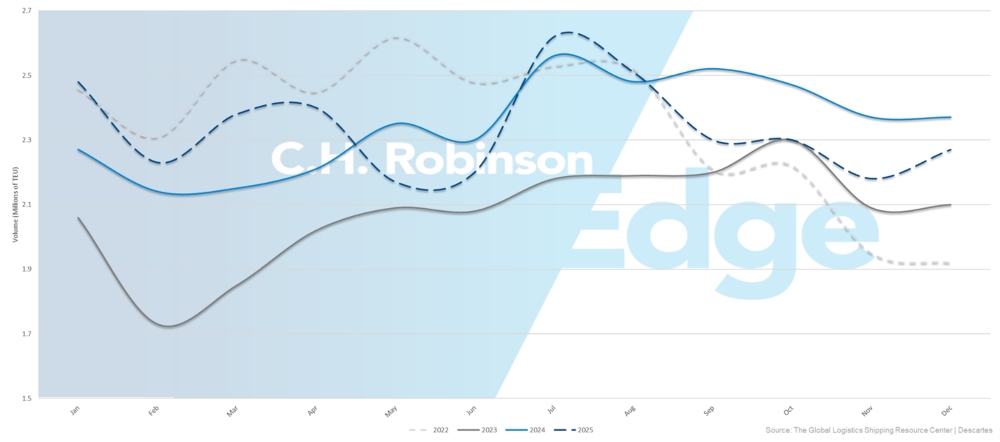

In December 2025, U.S. container imports reached around 2.2 million 20-foot equivalent units—a decrease of 5.9% compared to the previous year. For all of 2025, volumes ended up roughly 0.4% lower than 2024. This marks a change from the nearly 10% growth recorded earlier in the year, influenced by front-loaded shipments, a softening economy, and reduced consumer demand. Nevertheless, December 2025 was still the fourth-strongest December ever, illustrating that underlying demand remains stable even as it declines from peak levels.

2022–2025 U.S. container import volume (TEU)

Regional port congestion persists

Even with lower shipping volumes in February, congestion continues to shape operations across parts of the global ocean network.

Multiple north European hubs—including Hamburg, Rotterdam, and Antwerp—are facing slower operations, intermittent suspensions, and weather-related disruptions. These locations remain sensitive to vessel bunching and inland service issues, which can extend cargo availability timelines even when ocean transit is stable.

Congestion also persists in parts of Asia, particularly in major transshipment hubs. Industry sources have noted ongoing delays tied to yard utilization and congestion at critical nodes such as Singapore and Port Klang, where limited feeder frequency and post-Lunar New Year shipping needs may extend connection times and contribute to delayed cargo availability into March.

South America’s terminal performance varies. Ports such as Itajaí and Navegantes face congestion and disruptions, while Itapoá and Paranaguá deal with high utilization and slow turnaround. In contrast, Rio Grande, Rio de Janeiro, Imbituba, Vitória, and Fortaleza remain stable, highlighting a regional split between constrained and fluid corridors.

February looks calm because pressures are distributed

The forward-looking view suggests that February may feel steady, but not because the market is flush with capacity or insulated from pressure. Instead, the month is shaped by overlapping timing effects, targeted capacity management, and routing differences that create pockets of variability across Asia, Europe, South America, and North America.

Individually, these forces exert only limited pressure. Together, they compress the operating environment enough that flexibility, longer lead times, and thoughtful service-string selection take on greater importance than market indicators might suggest.

Planning ahead

February’s market favors slightly longer lead times and closer alignment on service-string selection. While a major change in strategy isn’t needed, plan now for post-Lunar New Year factory restarts and seasonal inventory build-up in late February and early March.

Network adjustments create regional pockets

February’s ocean market is being influenced less by broad demand trends and more by how carriers are configuring their networks at the lane and service-string level. This is leading to uneven space availability, wider ranges in transit times, and varying levels of operational reliability. In this environment, routing and service-string choices are a bigger factor in planning decisions.

Asia’s service patterns reflect controlled capacity, not surging demand

On major east-west trade lanes, particularly Asia–North America and Asia–Europe, carriers are continuing to employ selective blank sailings, tighter space allocation, and targeted deployment adjustments to keep vessels full. Rates in several lanes remain steady or slightly softer, with continued pressure on Asia–north Europe compared with the Mediterranean, reflecting differences in service density and port performance rather than demand shifts alone.

India subcontinent shows structural routing shifts taking hold

Several major Indian subcontinent services have resumed routing through the Suez Canal on select voyages. Although demand and stated capacity have not changed, this influences schedules, feeder connection times, and timing arrangements at hub ports.

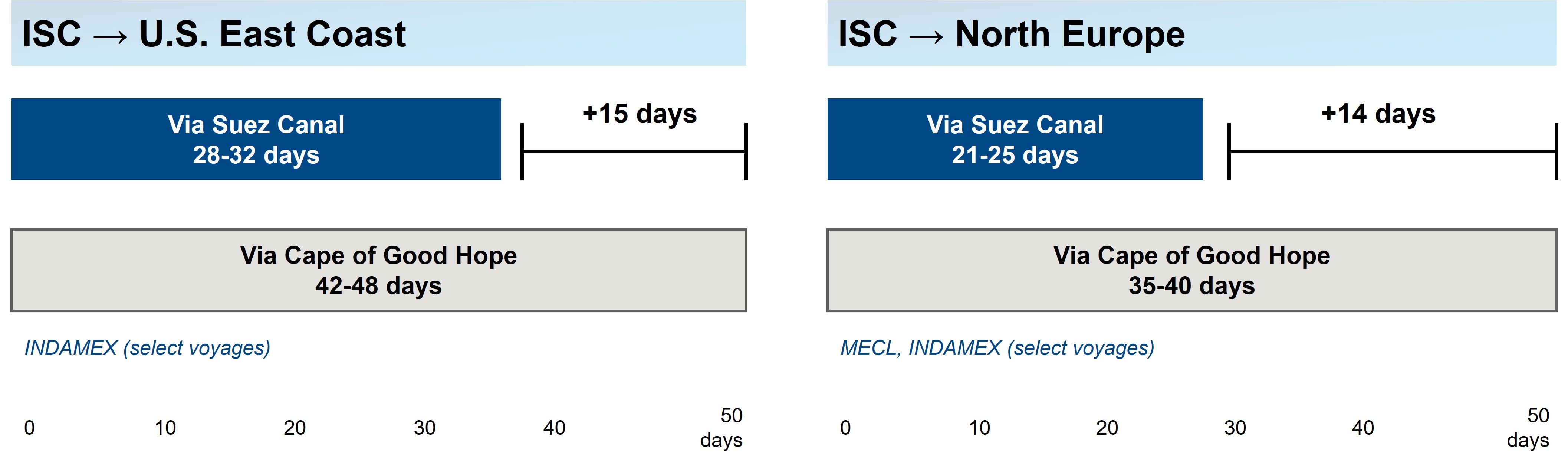

Suez vs. Cape of Good Hope transit time comparison

Select services resume trans-Suez routing, reducing transit times by ~2 weeks

The resumption of Suez Canal routing on select CMA CGM INDAMEX and Maersk MECL services reduces transit times by approximately two weeks compared to diversions around the Cape of Good Hope. For Indian subcontinent to U.S. East Coast, Suez routing offers 28- to 32-day transit versus 42–48 days via the Cape of Good Hope.

For Indian subcontinent to north Europe, Suez delivers 21- to 25-day transit compared to 35–40 days. This structural shift has significant implications for booking windows, inventory planning, and service-string selection through Q2 2026.

South America and Oceania present windows of flexibility

Several regions present areas with available space and competitive pricing, particularly when compared to the more regulated Asia trade routes. On the South America East Coast, shipping companies are seeking extra cargo by offering open capacity and consistently attractive rates for dry commodities, although certain ports still face inconsistent performance.

At the same time, Oceania continues to show strong year-over-year (y/y) demand, particularly for refrigerated shipments like grapes, while keeping capacity available on services such as Hapag-Lloyd’s AAXE and A3S rotations and Mediterranean Shipping Company’s (MSC) recently expanded KEA/Eagle service. These conditions may offer cost-efficient alternatives or rerouting opportunities for February cargo.

New service portfolio adjustments signal ongoing network diversification

Carriers are updating service design across regions in February:

- New Oceania routes connect Australia, New Zealand, and the U.S. East Coast

- Shuttle patterns and direct calls are being rebalanced in South America, shifting away from congested gateways toward more fluid ports

- Changes in vessel size and deployment on some Asia–North America loops

These updates increase routing options and may affect cargo flow through secondary ports in late Q1.

Planning ahead

Service configuration and lane-level space management may affect market conditions more than demand patterns. Asia’s capacity remains tightly managed, India subcontinent routing patterns are shifting structurally, and regions such as South America and Oceania are signaling pockets of flexibility. At the same time, inland constraints—such as chassis, equipment, and rail performance—continue to influence cycle time more than vessel schedules alone.

Understanding these asymmetries can help shippers make smarter routing choices and timing decisions as the quarter progresses. For more details, visit the Ports & Drayage section of this report.

Notable updates this month

Trans-Pacific rates decline even as pre-holiday activity picks up

General rate increases attempted early in the month have not held, with several carriers extending rate validity or reducing levels shortly after filing increases. This pattern suggests softer-than-expected demand is exerting more influence than seasonal pre-Lunar New Year lift. The same pattern may indicate carriers are prioritizing vessel utilization over sustained rate levels. Monitor mid-cycle rate adjustments closely, as these shifts appear to occur with limited notice.

North America export markets offer open space, but operational challenges remain

Outbound capacity from North America appears open across many regions, with carriers signaling willingness to negotiate on volume. However, certain lanes—such as the U.S. Gulf and West Coast to Europe—remain tight, with capacity constraints and service changes limiting flexibility.

Inland limitations add another layer: low-water restrictions in Montreal are reducing allowable load levels, and equipment shortages at key inland ramps such as NS Landers (Chicago) and NS Sharon (Cincinnati) continue to complicate execution. Given these variations, stay flexible and use advanced technologies that support timely adjustments as market conditions change.

Oceania demand and service expansion offer greater routing flexibility

Oceania is experiencing stronger demand than typical for early Q1, supported by seasonal refrigerated cargo—especially grapes—and steady dry cargo bookings. New rotations such as MSC’s KEA and Eagle service are expanding direct access to North America and Latin America, while Hapag-Lloyd’s AAXE and A3S rotations show solid capacity availability. This combination of rising demand and expanded service may offer more routing options than in other regions where capacity is constrained or heavily managed.

South America shows competitive pricing amid port-level variation

Despite ample available space and competitive market conditions, operational performance along South America’s East Coast varies significantly. Ports such as Rio Grande, Rio de Janeiro, Imbituba, Vitória, Salvador, Suape/Pecém, and Fortaleza are operating normally, offering fluid options for exporters.

In contrast, several key gateways are seeing more strain: Itajaí remains congested with limited calls; Navegantes is operating at roughly 65% utilization with average delays of about 10 days; and Itapoá and Paranaguá continue to face terminal pressure and weather-driven slowdowns. Pricing for commodities such as wood and tiles remains generally stable, although 20-foot equipment availability is tightening, prompting carriers to prioritize allocation.

Overall, the region continues to adapt effectively to shifting market conditions; however, being aware of specific port conditions is still helpful for planning exports, particularly when dealing with time-sensitive shipments.

Key takeaways

- Build a slightly longer booking window on Asia-origin cargo, especially through late February. Feeder frequency may remain limited into early March. This helps mitigate risk from missed cutoffs and slower transshipment flows.

- Validate port-specific conditions when routing through South America East Coast, where operational performance differs sharply: ports like Itajaí, Navegantes, Itapoá, and Paranaguá face congestion or weather-driven delays, while Rio Grande, Rio de Janeiro, Imbituba, Vitória, and Fortaleza remain fluid. This can meaningfully affect time-sensitive exports.

- Maximize open export space from North America, but watch inland operations closely. Although space exists, congestion remains on routes like U.S. Gulf and West Coast to Europe, with inland hubs—such as NS Sharon (Cincinnati) and NS Landers (Chicago)—still facing delays, chassis shortages, and slow cycle times due to metered releases.

- Leverage commercial flexibility in Latin America and Oceania, where open space, competitive pricing, and carrier appetite for volume create opportunities—supported by stable service in ports such as Rio Grande and expanded service offerings in Oceania. This can help diversify routings while other regions remain more constrained.

Actionable freight insights

Actionable freight insights